Inflections and Recoveries How New York City’s Real Estate Sector Has Recovered From Periods of Significant Decline

Since the turn of the century, unprecedented events including a terrorist attack, a once-in-a-lifetime financial crash, and now a pandemic have each significantly impacted the local economy. While the effects of 9/11 and the 2008 Financial Crash were unique, they might be able to offer insights into how quickly a downturn and recovery might take place. We are continuing to track markets that are ahead of us on the curve and will report on findings as it relates to our own path forward.

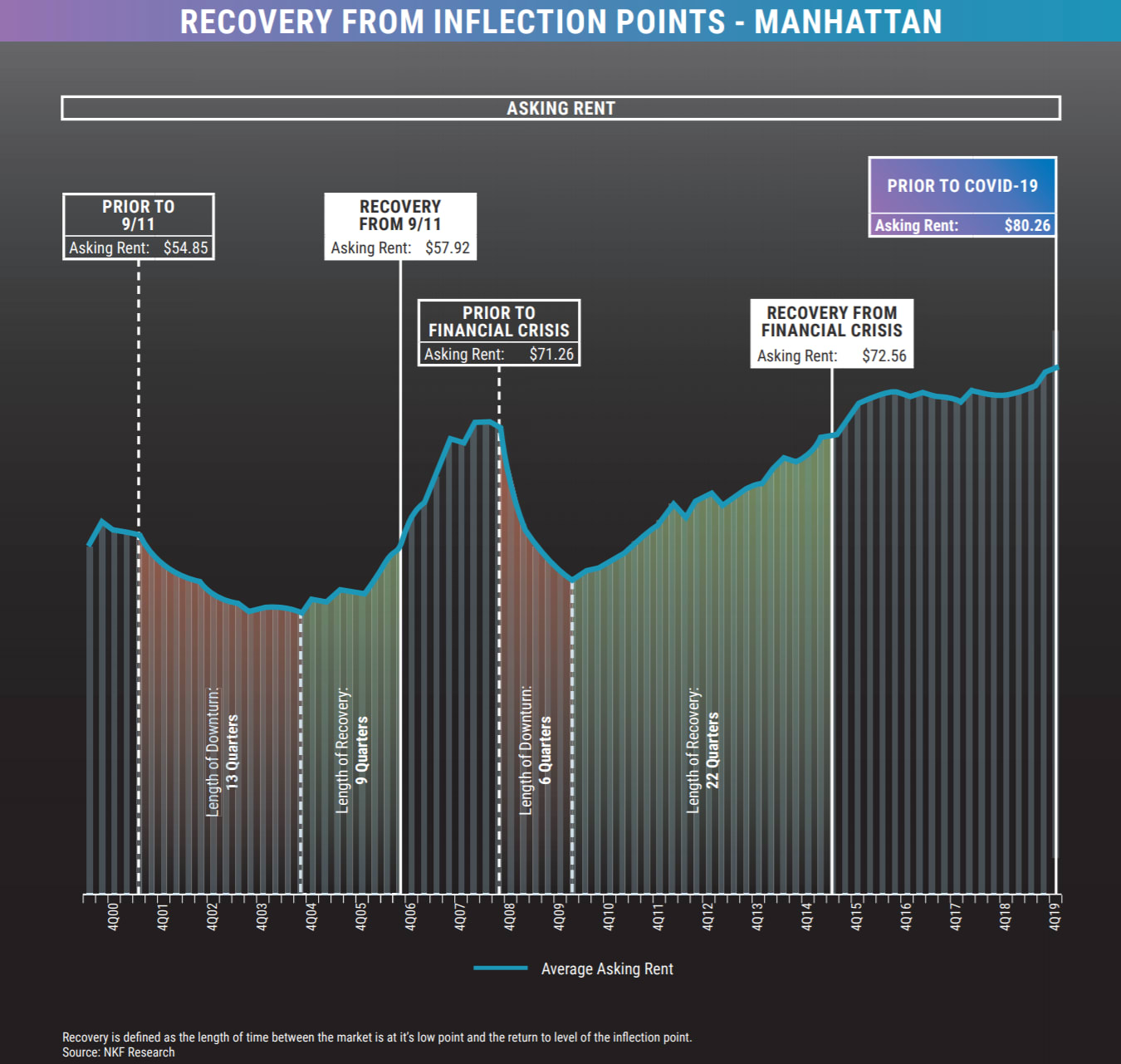

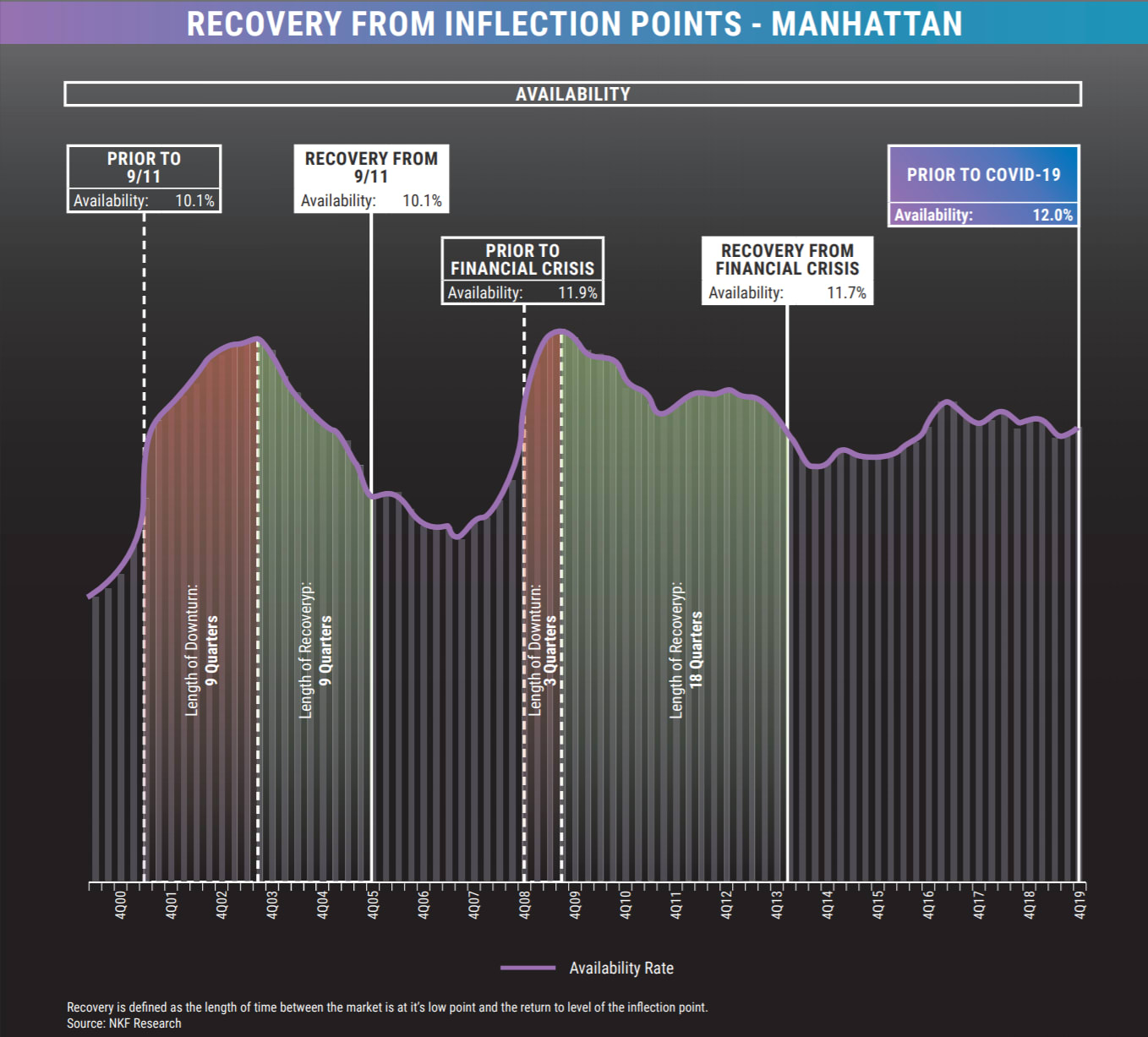

Q3 of 2001: Terrorist Attacks of September 11

Key Takeaways:

- While the Downtown availability rate hovered within 50 basis points of 15.0% in the 6 quarters preceding 9/11, the market was already seeing recessionary effects, with Manhattan availability increasing from 7.5% in 2Q00 to 10.1% in 2Q01. After 9/11, DT availability increased for 4 consecutive quarters and took 5 years to fall below 16.0%, reaching as high as 21.4%.

- Downtown average asking rents fell for 3 straight years after 3Q01, and did not return to pre-9/11 levels again until 1Q07.

- Overall Manhattan availability and asking rents recovered more quickly than the Downtown market. Manhattan took approximately 3 years for availability levels to recover and 5 years for rents.

- Downtown leasing velocity declined from 2002 through 2005, before fi nally increasing and eclipsing 5 MSF in 2006.

- The average leasing velocity from 2002 through 2005 was just 3.5 MSF.

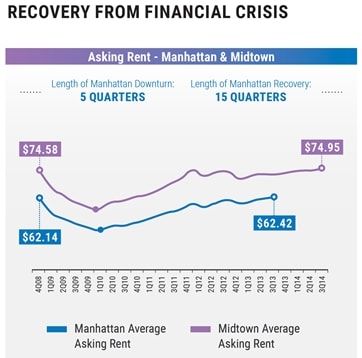

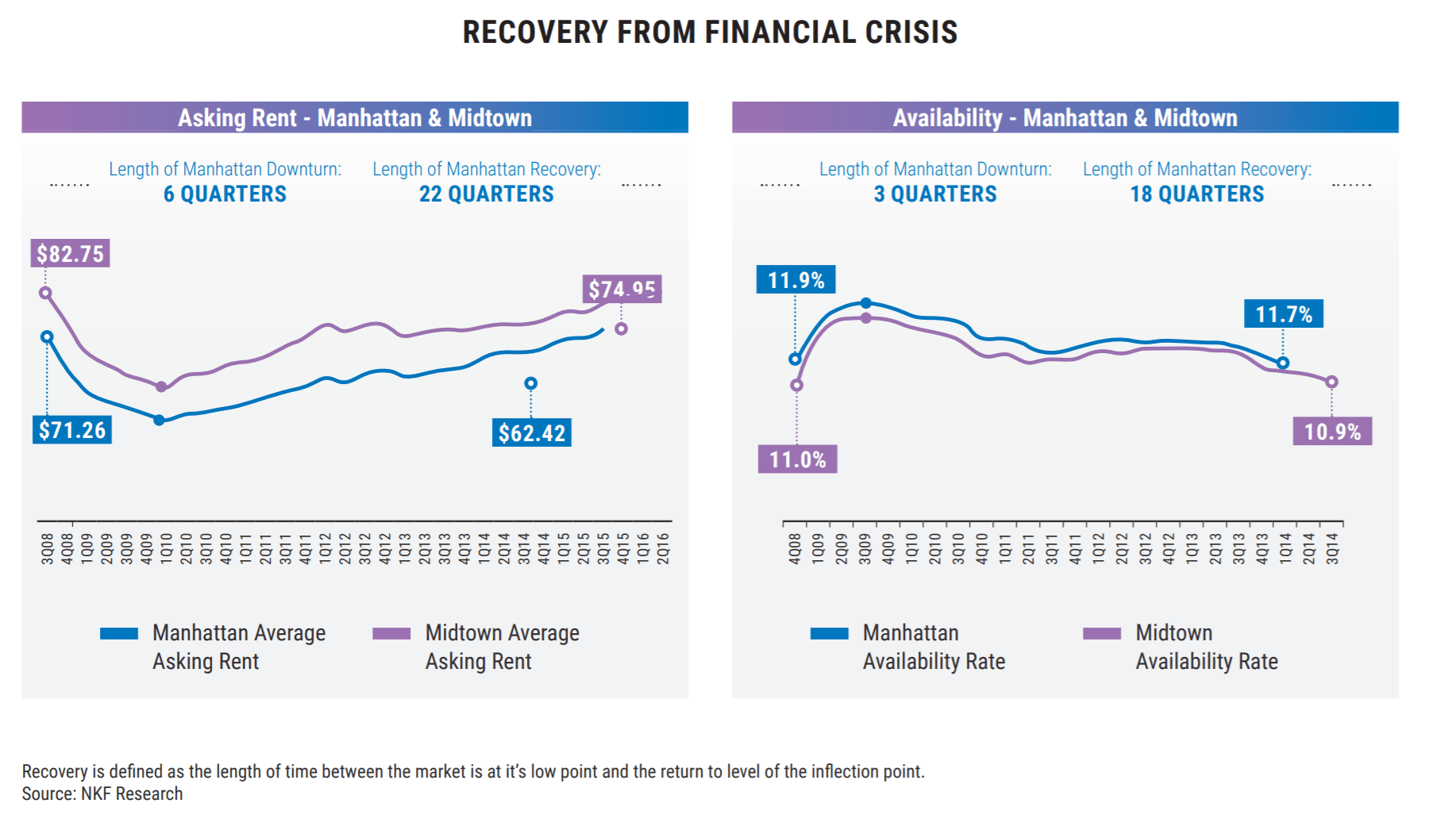

Q4 of 2008: Global Financial Crisis

Key Takeaways:

- After reaching the market’s peak in 2008, Manhattan asking rents dropped by as much as 32.6% from $71.26/SF in 3Q08 and took 7 years to reach that level again.

- Although velocity increased in the years after the fi nancial crash, with year-over-year improvements through 2011, the rate of renewals as opposed to relocations was responsible for the jump earlier in the cycle.

- In the years leading up to the crash, there were 16.6 MSF of renewals (‘03-’07), with 29.2 MSF in the fi ve years following (’08-’12), as tenants looked for stability and the lower rents offered at that time.

- The Midtown availability rate skyrocketed 45.8% in just one year from 3Q08 to 3Q09. While rents have returned to and surged past their prior levels, availability has not yet fallen below 10.0% in the 11+ years since. It stood at 9.6% in 3Q08.

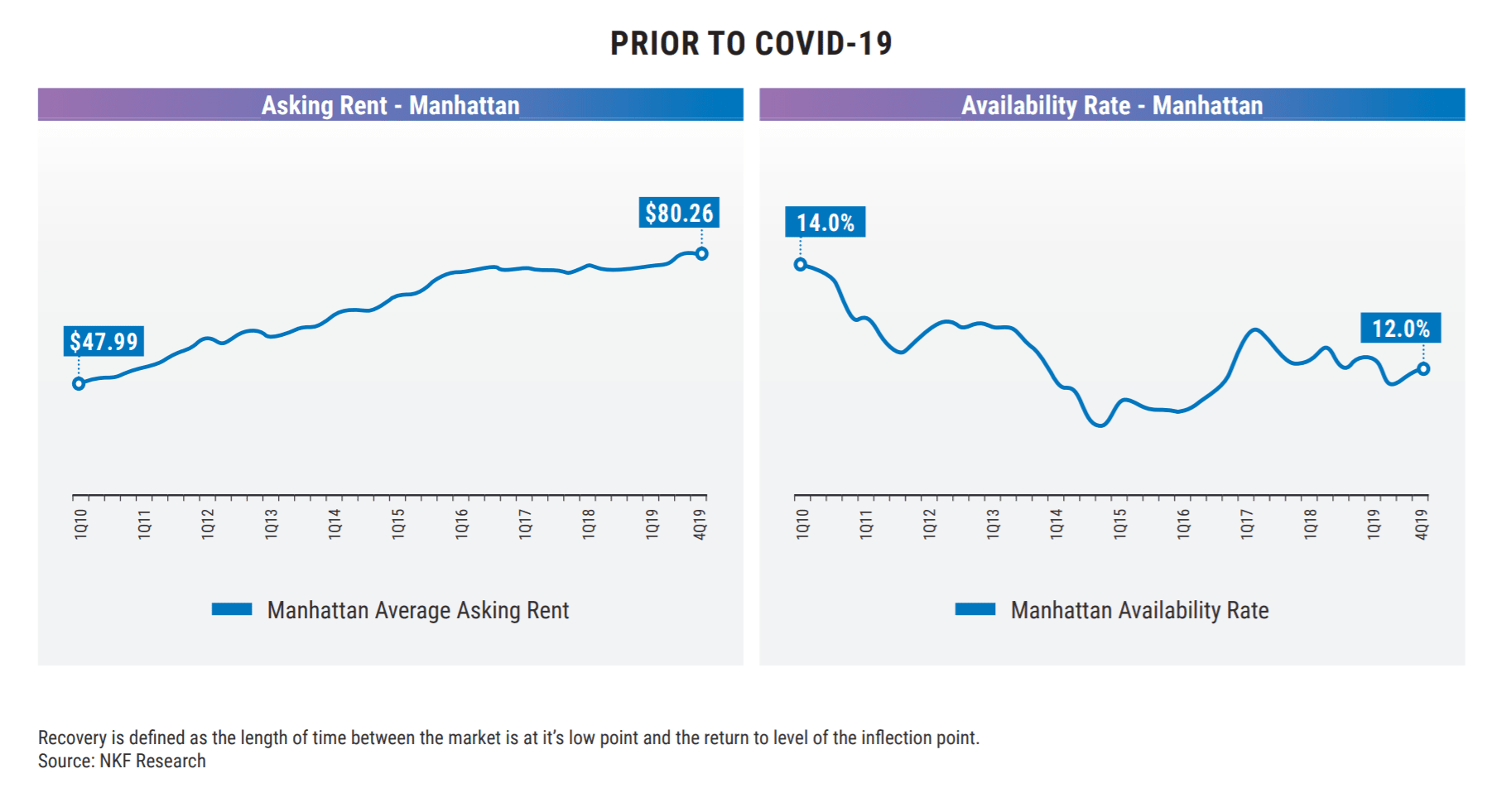

Q1 of 2020: Covid-19 Outbreak

Key Takeaways:

- As the virus reached New York, the market was coming off two consecutive years of record leasing activity, including 50 MSF of velocity in 2019, and began to show signs of tapering off that record pace. Q1 projections show leasing activity at approximately 6 MSF.

- The availability rate has hovered around 12.0% for the past 3 years. Previous projections had already called for an increase in overall availability over the next several years and this downturn will likely cause additional pressure to the market.

- Asking rents had established cyclical highs in recent quarters closing 2019 at more than $80/SF. Reductions are expected as landlords will work to lease up anticipated additional available space.

- After non-essential construction work was halted, it’s expected that delays will occur for the 16.2 MSF of offi ce space under construction in Manhattan.

Share: